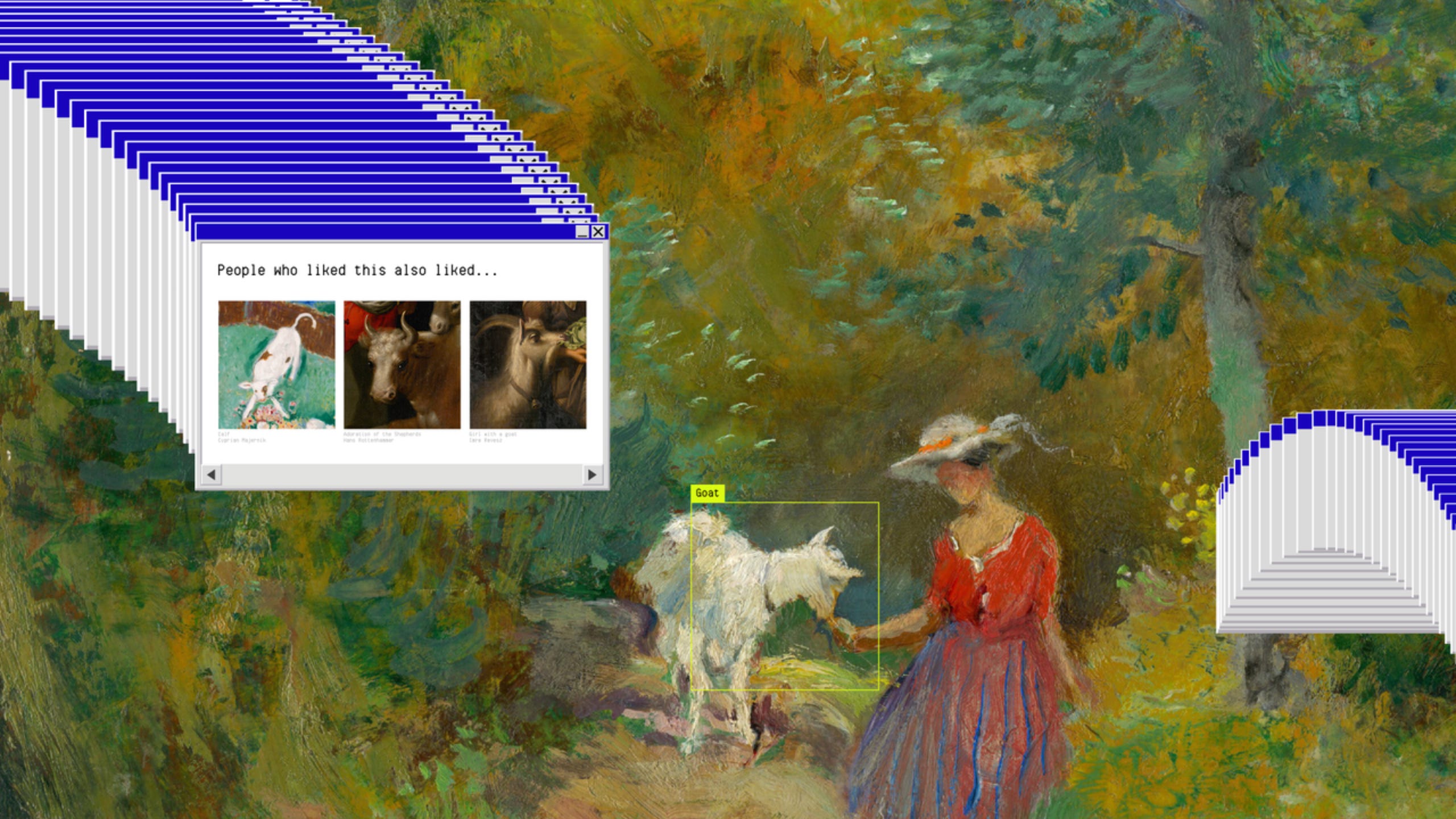

Bubbles pop eventually.

When the dot-com bubble popped in 2000, it caused the worst decline in the NASDQ’s history, dropping by more than 70%. Many companies that had so confidently slapped ‘.com’ on the end of their names suddenly had to face a reckoning, and many did not survive.

They did not survive because aesthetics would only get them so far. The shiny new object, which back then came in the form of a website on the world-wide web, would eventually need to prove its worth.

A bubble popping represents a reversion back to reality and fundamentals, and that is when the promises and predictions of technology are really tested.

And one of the more significant players carrying out this testing are investors. Having a cool product with potential is fine on Day 1. But on Day 2, investors are looking at the prospect of their returns. They want to know what they will end up getting out of it all.

Google was no exception to this.